Corporate Defaults and the Dangerous Rise of "Shadow" Defaults

Chaos Breeds Chaos

Note: This newsletter contains information for educational purposes only, and the content below should not be considered financial advice to readers. We published a brand new short recommendation for our clients. If you would like to become our client, email laks@unicusresearch.com…

The United States is losing its economic dominance, thanks to irrational trade wars. As the “headline distractions” continue to trigger market volatility, it is critical to remember that “the stock market is not the real economy.”

The real economic challenges are deafening: the persistent rise in inflation, shrinking consumer credit, increasing corporate defaults, and deteriorating asset-backed securities for commercial mortgages and auto loans, as well as spiking student loan defaults and public/private credit risk, are weighing down consumers and corporations alike.

Political and economic instability can increase the risk of corporate defaults and bankruptcies. The instability will bring the lingering systemic issues to the surface.

A perfect economic storm is brewing.

SUMMARY

Expect a continued spike in distressed corporate defaults, not “hard” defaults.

50% of natural resource firms show severe signs of default risk.

3% of regional banks show several early signs of default risk (we recommend three regional banks as a short).

29% of transportation firms show early signs of default warning risk.

35% of technology firms show severe early default risks.1

Our machine learning team is creating a model to monitor corporate and distressed defaults constantly. We will update when we release the products.

Corporate Defaults 2025 and Beyond

Americans are highly pessimistic about the economy.

Consumer confidence and corporate defaults have a complex and often inverse relationship. While not a direct causal link, lower consumer confidence can lead to decreased consumer spending, negatively impacting a company's revenue and profitability, increasing the risk of default.

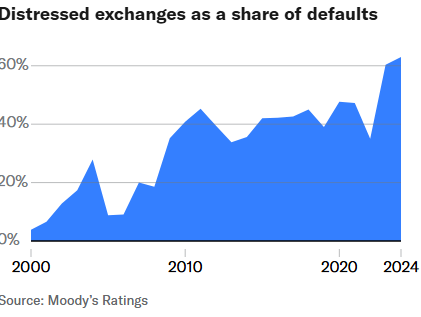

The global corporate defaults ticked lower in 20242, to 145 from 153 in 2023. Nearly 60% of the defaults in 2024 were distressed exchanges.

High interest rates and stubborn inflation have depleted consumer savings and lowered discretionary income, particularly for lower-income consumers. The consumer/service sector led the default tally for the fourth year with 33 defaults in 2024, while the leisure time/media sector had the highest default rate (4.89%).

While the number of defaults fell slightly in 2024 (to 145, from 153 in 2023), the number remained elevated--largely because of distressed exchanges. The number of distressed exchanges rose to its highest level since 2008, accounting for 59.3% of defaults.

One reason for the rising percentage of distressed exchanges and the high level of repeat defaulters is financial sponsors’ desire to maintain control of their portfolio firms while attempting to reduce debt.

Thus far, 2025 has seen higher corporate defaults and re-defaulters. The number of year-to-date global corporate defaults rose by nine to 26 in March 2025, but the year-to-date count is below the 37 recorded for the same period in 2024 and the five-year average of 29.

Re-defaulters accounted for five defaults in March, or 56% of monthly defaults. The share of re-defaulters reached 42% in the first quarter of 2025, the highest level since the first quarter of 2019, when it was 48%.

The S&P expects the global corporate default to spike in 2025. From automobiles to airlines, the manufacturing supply chains have frozen. Consumers are postponing their spending until they have a clearer picture of the economy. Additionally, alongside the slow US GDP growth, we expect unemployment to spike (lag-catch up) over the next few quarters.

Consumer Confidence Reflects in the Corporate Defaults

As we have shared in our short recommendation reports to our clients, consumer confidence is reflected in corporate earnings and consumer credit, especially for the lower-tier consumer base, which has dried up.

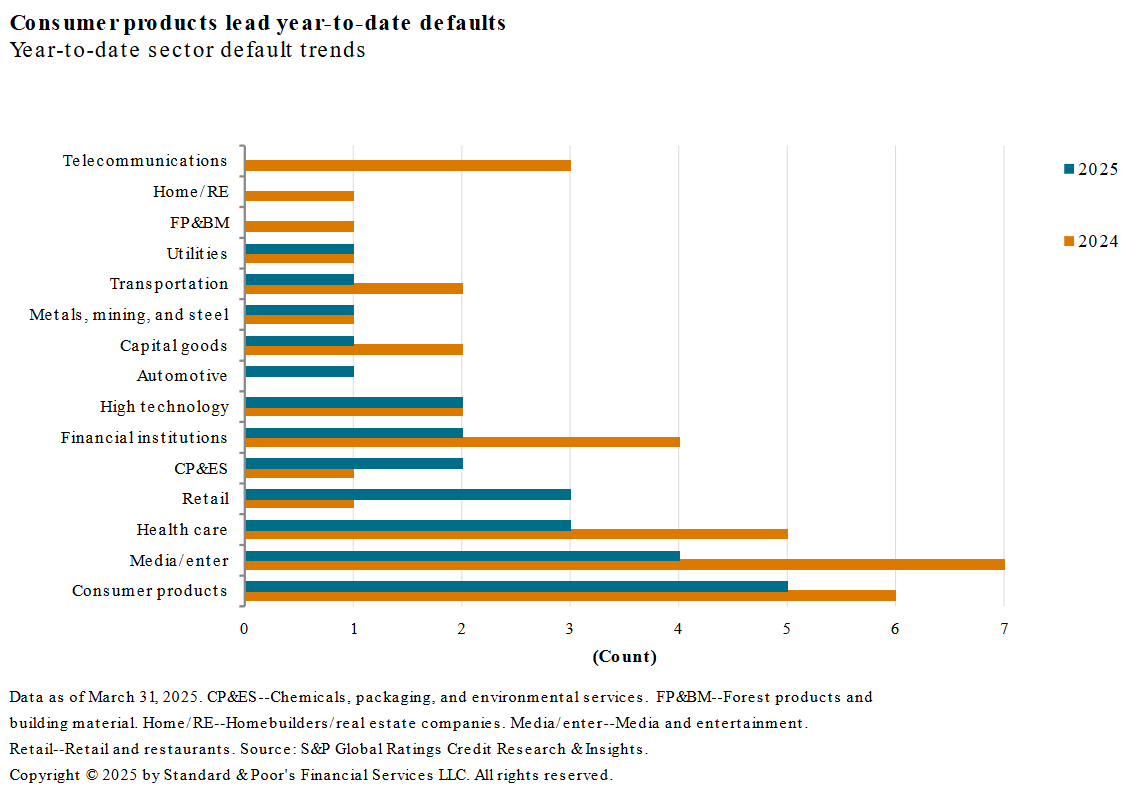

The three sectors that accounted for most defaults (46%) in the first quarter of 2025 include

Consumer products (5)

Media and entertainment (4)

Health care (3)

Four of the nine defaults in March occurred in the high technology sector as well as the retail and restaurant sector. Despite declining interest rates, issuers in these sectors still face higher average refinancing costs.3

Financing conditions remain challenging for companies with highly leveraged structures and weak operating metrics because these structures constrain their access to capital markets in the current environment. Additionally, consumer-sensitive sectors suffered tepid consumer demand.

Credit strain on borrowers could intensify, given tight liquidity and higher borrowing costs. This raises the likelihood of more defaults.

Trade tensions are threatening previously favorable credit conditions for most borrowers. Market volatility and increasing investor risk aversion pose the most imminent risks to credit in the current environment. Borrowers must pay up for financing, and, worse, some lower-rated borrowers could be shut out of the capital markets.

The Rise of “Shadow” Defaults

After we reviewed the data from the big three credit rating agencies, it is clear that the impending corporate defaults will rarely be “hard defaults,” missed payments, or bankruptcies; the expected heightened default risk is more likely to manifest itself in more distressed restructurings. Restructuring a debt contract by extending maturities and modifying other material terms, especially under financial duress, is often considered an event of default - or what we call “shadow defaults.”

Moody’s Ratings4 reported that in 2024 distressed exchanges accounted for about 63% of defaults, the highest annual share on record, with data going back to the 1980s. Moody’s Ratings noted that it expects distressed exchanges to remain elevated in 2025, especially among private equity (PE)-owned companies, as PE sponsors will try to extend their options and extract value at the expense of lenders. It also expects some companies to re-default if their recent debt exchanges did not sustainably reduce their debt burdens.

RED FLAGS in the Credit Market

According to Moody’s5, as of the end of January 2025, 32% of US public companies had severe EWS signals, meaning that their implied ratings had deteriorated over the past year and their probability of default exceeded their industry sector trigger levels. Including companies with high early warning signals, 37% of US public companies are flagged as notably risky, surpassing the April 2020 high when 35% of US public companies showed high or severe early warning signals as the Covid-19 pandemic swept the economy.

From Moody’s data analysis tracker

www.spglobal.com/ratings

www.spglobal.com/ratings/en/research/articles/250416-default-transition-and-recovery-trade-tensions-could-reverse-decline-in-corporate-defaults-13473883

https://www.moodys.com/web/en/us/insights/data-stories/us-corporate-default-risk-in-2025.html

https://www.moodys.com/web/en/us/insights/data-stories/us-corporate-default-risk-in-2025.html