Breaking Down BNPL

The Leverage is the New Age Slavery

Note: This newsletter contains information for educational purposes only, and the content below should not be considered financial advice to readers. We published a brand new short recommendation for our clients. If you would like to become our client, email laks@unicusresearch.com…

Note: It is dangerous to give a sober person alcohol.

It is dangerous to provide credit access and buy now, pay later (BNPL) access to individuals who lack fiscal discipline.

Be In the Know

It is crucial to comprehend the intricacies of Buy Now, Pay Later (BNPL) and its operational mechanics.

BNPL provides credit access to financially vulnerable consumer groups. Consumers are feeling the squeeze from economic uncertainty and are increasingly turning to financing essential purchases, such as groceries.

An April survey from Lending Tree1 shows an increase in Americans using buy-now, pay-later services for groceries—25% this year compared to 14% in 2024.

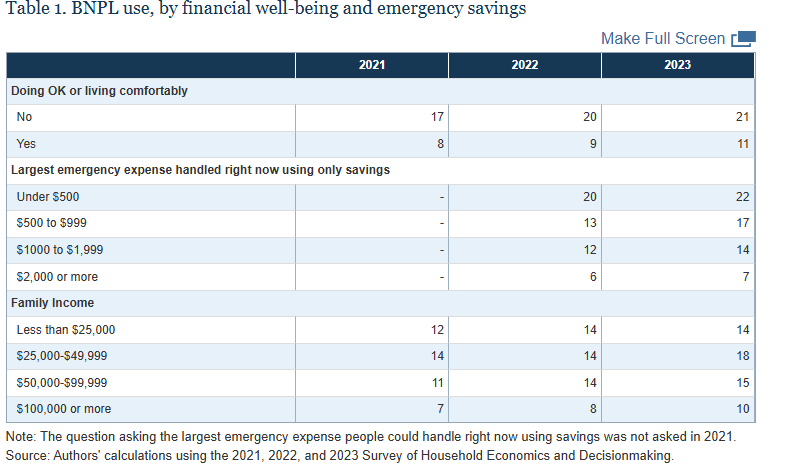

The Federal Reserve conducted a recent survey with a relatively large sample and scope of the Survey of Household Economics and Decisionmaking (SHED) to examine BNPL use by the intersection of race/ethnicity and gender, as well as to explore how BNPL use relates to people's financial circumstances.2

Findings

Adults who report lower overall financial well-being and those who appear liquidity or credit constrained were not only among the most likely to use BNPL, but most of these consumers also indicated that they used BNPL because it was the only way they could afford to make the purchase.

In contrast, those with higher financial well-being and more financial resources were less likely to use BNPL in the first place, and those who did, typically did so to spread out payments or to avoid interest charges.

Adults with smaller amounts of emergency savings and those with low- and middle-income were also more likely to use BNPL.

More users see BNPL as a “bridge” to their next paycheck. 33% say this, up from 30% last year and 27% the year before. High earners, men, younger Americans and parents of young kids are among the most likely to say so.

More than 6 in 10 BNPL users (62%) incorrectly believe making on-time payments on BNPL loans helps your credit score. Only 13% say they don’t help your credit score, which is correct, while 26% aren’t sure. Men and high-income earners are among the most likely to believe this falsehood.

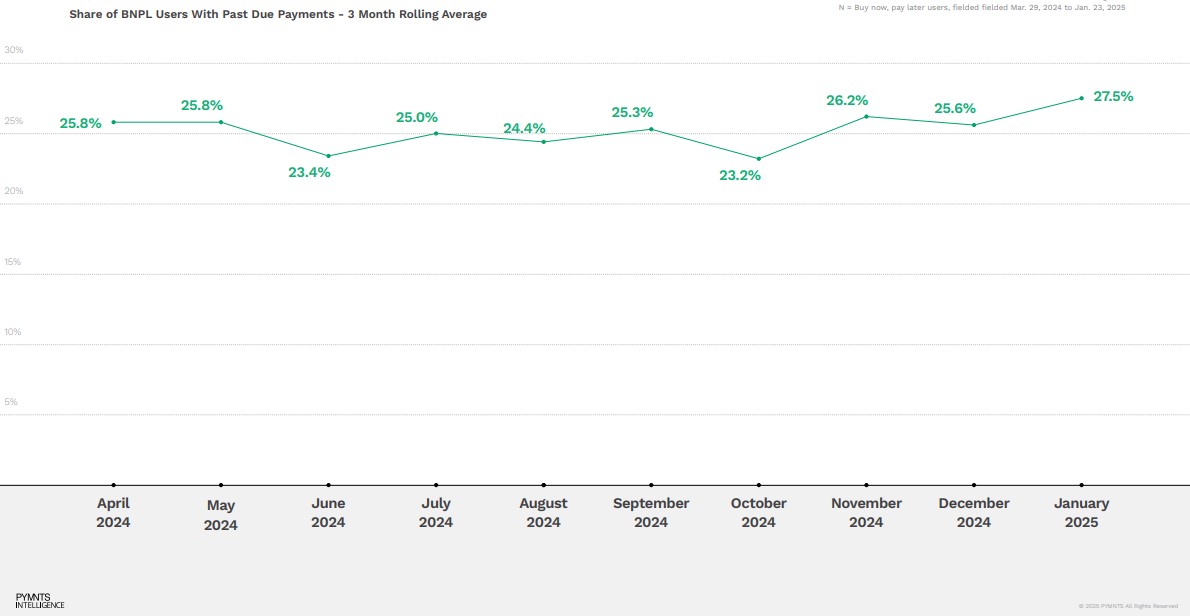

BNPL Delinquencies Spike

According to the new PYMNTS Intelligence data, shows a recent sharp rise in BNPL delinquencies.

RED FLAG#1

As of mid-to-late January 2025, nearly 30% of all BNPL loans were past due, a PYMNTS survey of 2,330 U.S. consumers over Jan. 14 to Jan. 23 shows. That represents a nearly 54% increase on the previous month, when 19.4% were delinquent. But it’s below the 33.3% rate for November 2024. Delinquency rates vary widely from month to month, according to the data, which PYMNTS began tracking in April 2024.

RED FLAG# 2

Default occurs when a borrower fails to meet a loan’s repayment terms, prompting the lender to give up on collecting and write off the losses as a charge-off 180 days or more after the account is past due.

Most BNPL providers do not turn over uncollected balances to a debt collector, given the small balances typically left on those loans, but will refuse to extend credit to them in the future, often on short notice.

Effective April/May 2025, BNPL lenders began to report defaults to credit rating agencies.

Schematics of BNPL

While there’s often no interest charged on BNPL purchases, borrowers who miss payments face late fees and charges ranging from a couple of dollars to up to 25% of the total purchase price from some providers. The total cost can add up quickly, especially if their payment is linked to a debit card or bank account with insufficient funds. Customers who default on repayments can see their negative standing sent to credit scoring agencies and find their history and scores dented

How BNPLs are Funded? Aka - Who bears the Risk?

The Pay Later ecosystem's business model involves a complex flow of funds and a monetization structure. Stated, Pay Later providers function as an intermediary between the consumer and the bank, moving money from the consumer’s account to the merchant.

A BNPL consumer typically pays a portion of the purchase price upfront. But the merchant still receives full payment at the time of purchase, which means the difference must be funded. Individual BNPL providers manage that funding differently.

Balance Sheet: Some BNPL providers provide funding directly from their balance sheets, either through cash on hand, or via lines of credit provided by credit facilities.

Credit Facilities: Many BNPL providers rely on credit facilities to provide credit lines to fund BNPL loans.

Credit Card Networks: A virtual card that runs over traditional card rails is generated for the exact amount of the transaction at checkout. That virtual card is used to pay the merchant instantly for the purchase and collect funds from the consumer over time, consistent with the terms of the loan.

Merchant-Supported Financing: In some instances for large dollar purchases like furniture or dental work, the merchant may provide the funding, using third-party financing providers to underwrite and fund the loans.

Loan Sales & Securitization: Some BNPL providers sell their loans to institutional investors or securitize them into bonds to free up cash for new lending.