Inflation Considerations

Access our track record: https://www.unicusresearch.com/track-record.

Schedule intro. call: https://www.unicusresearch.com/schedule-a-consultation

See Unicus Research’s previous discussion on inflation.

March Newsletter – Inflation Nation

August 22, 2022: Idiots and Inflation

December 2022: Inflation is getting worse, and the Taylor rule

April 2023: The Paul Volcker Shock 2.0

August 2023: Inflation and Recession

September 2023: The Economic Impact of the Resumption of the Student Loan.

September 2023 Inflation, Recession, and Stagflation

Inflation – it's still with us.

What are the components of an economy that drives inflation?

The three sisters of inflation are

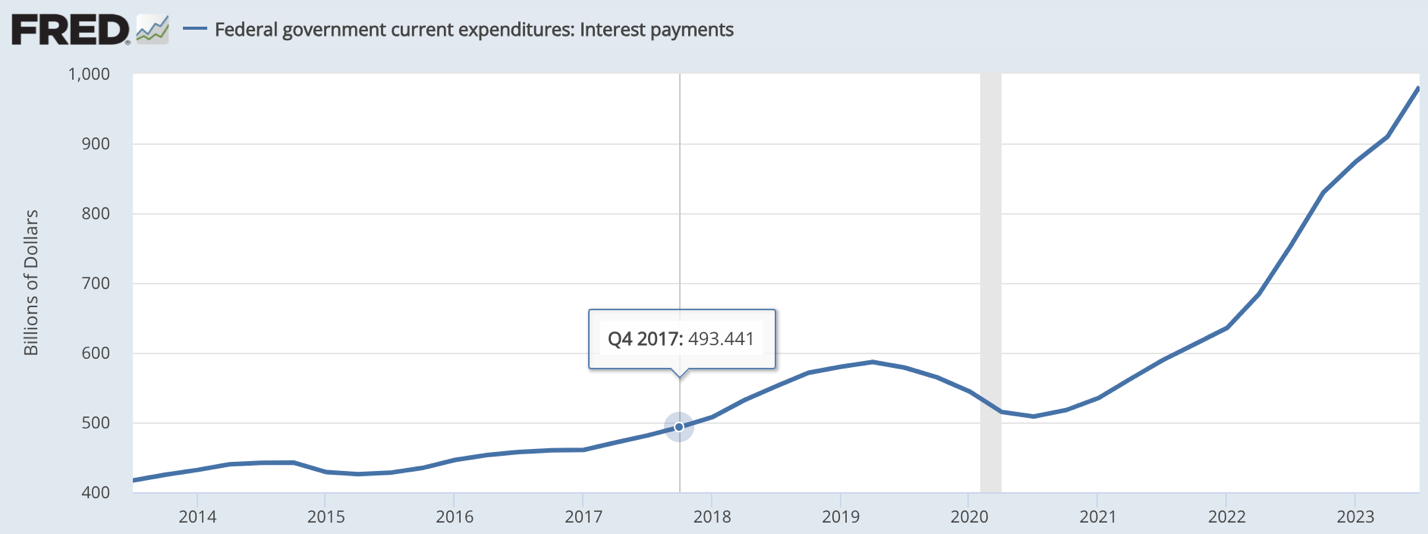

Government Spending

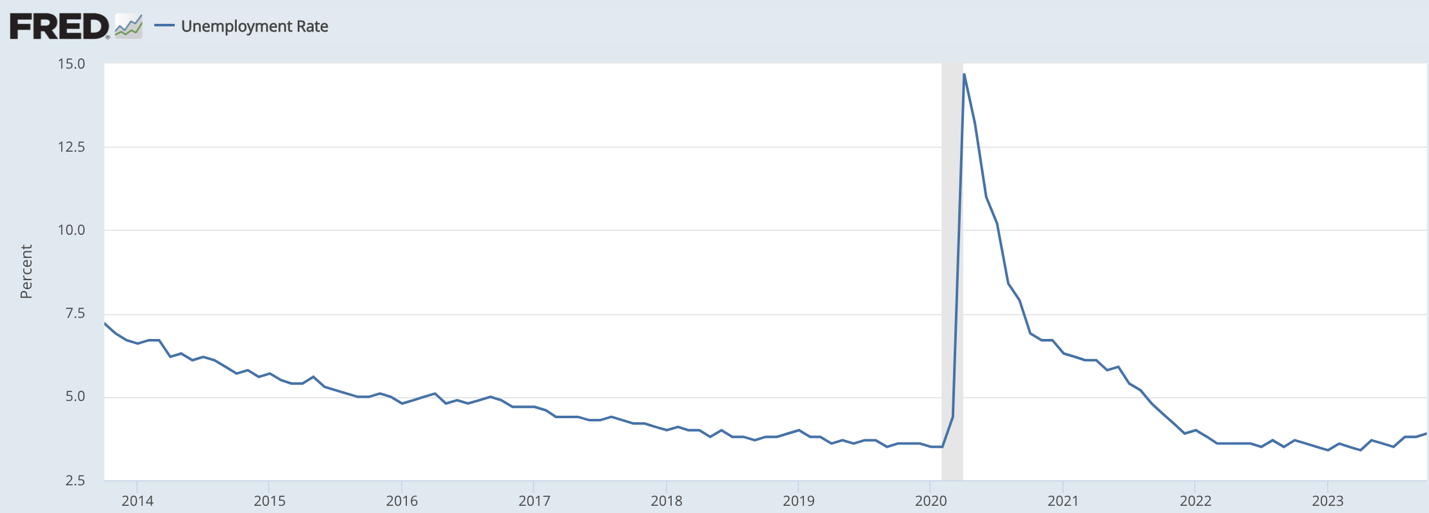

Unemployment

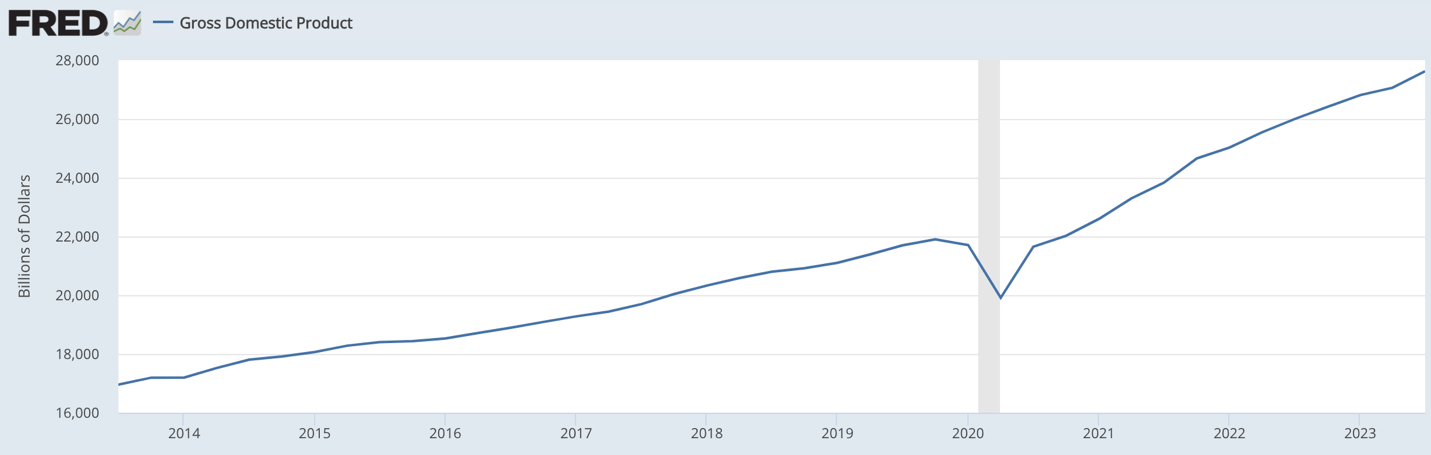

GDP growth.

But you say, “Heh, these are all interrelated! My answer is, “Yes, that's why I call them the three sisters” – sisters are related, aren’t they?

So, how do the three sisters work together?

Government Spending

Milton Friedman famously said: “Inflation is always and everywhere a monetary phenomenon, in the sense that it is and can be produced only by a more rapid increase in the quantity of money than in output.” Of course, we all know the driver of the quantity of money is government spending, and wow, have they been spending!

Spending spiked to deal with the economic consequences of the lockdown orders. But we both expanded our spending while crushing our GDP. As the economy rebounded – the US kept spending. Also, the spending was not regular spending but billions of dollars in aid that hit the consumer’s pocket. Did the consumers spend? Yes, the consumers did a great deal of spending. The spending drove up prices on several items, particularly Chinese high-technology goods that were scarce because of shipping constraints. So money flowed, and the government and the consumers – consumed.

One can clearly see the spike impact of the lockdown stimulus on the debt as a percent of GDP. While it reduced some, it has not reduced enough. The rule of thumb is that the US debt should hover around 100% or less of GDP to reduce the chances of inflation.

The US government's only control mechanism is to hike interest rates to mop up extra liquidity, and it does this by raising interest rates. The US is spending more, and more has to be paid to be able to spend.

This is the “Checkbook Therapy” model of debt. You feel bad or need to buy votes, so you spend more. Yet your mood and the voters need more and more simulation, so you shop more and more. There comes a time when the checkbook is empty, and the Checkbook Therapy becomes Credit Therapy. In time, unless there is an intervention, you spiral into bankruptcy.

The Federal Reserve has a bit of problems as well. “The most recent data show that the Fed owes the Treasury over $48 billion, which exceeds its total capital. The Fed, by common standards, is insolvent.”

The more borrowed over 100% of GDP tends to initiate inflation, which requires more debt if the spending levels are not addressed. The stimulus therapy goes from spending capital to auguring into debt.

Unemployment

When the economy is strong and unemployment is low, tight labor markets tend to increase inflation as employers must increase wages to attract and retain workers. This reinforcement loop of inflation driving wages driving inflation is the wage-price inflation spiral.

So, how did the US avoid the wage-price inflation spiral for the last several decades?

It is worth clicking on the link and reading the exchange in full.

Jarvis: “Historically, most economic expansions fade after this long. How confident are you that our economy won’t slip back into recession in the near term?”

Yellen: “... I think it’s a myth that expansions die of old age. I do not think they die of old age. So the fact that this has been quite a long expansion doesn’t lead me to believe that ... its days are numbered.”

Yellen is wrong — and she has a lot of company. It is an amazing reality that, among economists, the faith in the possibility of endless expansions has survived the 2008-09 financial crisis and the Great Recession.

Large “facepalm” by your author and editor. It might explain the nonsense statement: “Inflation is transitory.” It must have emanated from her lack of mental acuity and/or her being a diehard Keynesian.

Any bit of economic research will show that the rise of free trade agreements such as NAFTA and the reduction of tariffs under WTO accords have kept the lid on wages. Labor, capital, or regulations get too expensive, and the work can be shifted to another country. What are the most common items imported from Mexico? In order of value, it is vehicles, auto parts, electronics including major appliances, crude oil, medical instruments, beer, and plastics. What is the major expense to all the items, excluding petroleum? It is labor, then regulations. The same applies to nearly all imports from China, India, Vietnam, Bangladesh, and others. The cost differentials are the time from order to delivery, transportation, and duty. If those are, in the aggregate, lower, the jobs move overseas.

Trade has kept the lid on the wage inflation spiral.

How is that changing? It is changing because of China's actions during COVID-19, the shutting down of supplies for months and months. The absence of parts and supplies damaged or closed many businesses. In this time of conflict, China and other nations have used Western nations' dependency on their exports as leverage. Think US computer chip dependence on overseas and hostile suppliers and Germany’s dependency on Russian natural gas. So what has happened? Many companies have chosen to onshore the manufacturing of critical items back to the West. The trade buffer on wage increases has evaporated for the time being. As long as unemployment remains under 4.5% to 5%, the wage-price inflation spiral will continue contributing to inflation. A hint that the upward pressure on wages will continue will be the aggressive wage and benefit increases demanded by unions across the US.

GDP

The US is a resilient nation. We are a nation of tinkerers and creators of opportunity. Experts had predicted a US GDP growth for 2023 of 2.2%. Ha! In Q3 of 2023, it was a kick butt +4.9%.

The increase in Q3 reflects increases in consumer spending and inventory investment. Imports, which are a subtraction in the calculation of GDP, increased. Emphasis added. US imports increased, but GDP still accelerated to +4.9%! As amazing as it is, the GDP growth rate is inflectional as it reflects demand on wages and capital.

Analysis

The effective Fed Funds rate and the Fed Funds rate suggested by the Taylor Rule have almost converged. While we expected another .25% increase at the last FOMC – it did not happen. What did happen is the market rates for money increased and “covered the spread.”

Do we still see a recession? Yes, we do. It will be in different sectors. Lenders and owners of office space and light industrial space will be most hurt. This will be followed by general retailers, automotive and appliance dealers, entertainment, residential real estate services, non-industrial construction, and leisure and hospitality, especially restaurants. Shipping volumes are (off 4 to 8% from last year, with expenditures off 24%) across the US, foreshadowing the downturn. What will remain and do ok will be the sins stock, guns, liquor, and tobacco. The high-tech manufacturing sector will slump.

For a more detailed company or industry sector analysis, please contact Unicus Research LLC.

L. Burke Files CACM DDP Sr. Researcher

And Advisor to the founder

Uniucs Research, LLC

Weekender Music

California Ska – this is great.

A classic and soulful

You hit it, inflation has stopped increasing, and the smell of a recession is already in my nose.